When it comes to understanding mortgage rates in Canada, one key factor often discussed is the bond yield. Bond yields, particularly those associated with government bonds, play a significant role in determining mortgage rates offered by lenders. This article explores the relationship between bond yields and mortgage rates, how they impact each other, and why it’s crucial for potential homebuyers and homeowners to pay attention to these financial instruments.

What Is a Bond Yield?

A bond yield refers to the return an investor receives from holding a bond. Bonds are fixed-income securities issued by governments or corporations to raise capital. In Canada, government bonds, especially the 5-year bond, are closely monitored as they are tied directly to mortgage rates. When bond yields rise or fall, mortgage rates tend to follow suit.How Do Bond Yields Influence Mortgage Rates?

Mortgage rates in Canada, particularly fixed-rate mortgages, are often influenced by government bond yields. The most common bonds tied to mortgage rates are the 5-year and 10-year government bonds. Here’s how it works:- When Bond Yields Increase: Lenders adjust their mortgage rates higher to match the increase in yields. This adjustment ensures that their mortgage products remain profitable.

- When Bond Yields Decrease: Lenders may reduce mortgage rates to align with lower bond yields, providing a more competitive offering for borrowers.

Example of Bond Yield Impact on Mortgage Rates

Consider a scenario where the 5-year bond yield is currently at 2%. If the yield rises to 2.5%, lenders might increase their 5-year fixed mortgage rate from 4.5% to 5% to maintain a profitable margin. Similarly, if the bond yield drops to 1.5%, lenders may lower their rates to 4%, offering cheaper borrowing options to homeowners. For example:| Bond Yield | Mortgage Rate (5-Year Fixed) |

|---|---|

| 2.0% | 4.5% |

| 2.5% | 5.0% |

| 1.5% | 4.0% |

Why Bond Yields and Mortgage Rates Are Closely Tied

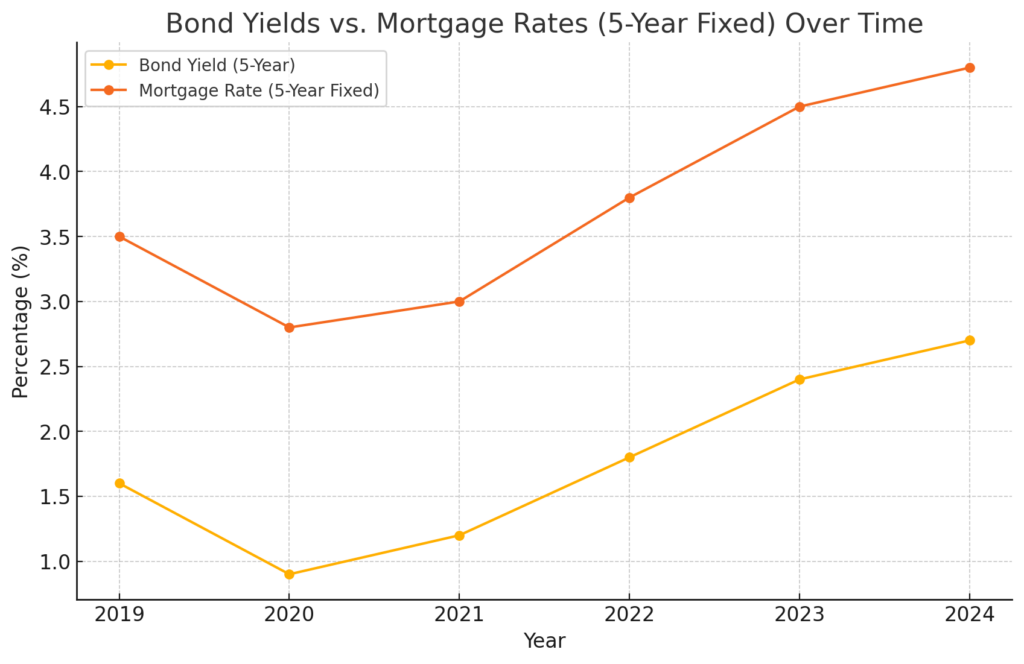

Lenders use bond yields as a benchmark for setting their mortgage rates because bonds and mortgages are both forms of debt securities. Both instruments react similarly to changes in economic conditions and central bank policies. For example, if the Bank of Canada raises interest rates to curb inflation, bond yields generally rise, leading to higher mortgage rates. Conversely, when the central bank lowers rates, bond yields typically fall, resulting in lower mortgage rates.Chart: Bond Yields vs. Mortgage Rates Over Time

Figure: Bond Yields vs. Mortgage Rates (5-Year Fixed) Over Time